Demutualization of Blue Cross of LA Raises Serious Questions of Fairness

August 31, 2023

August 31, 2023  0 Comments

0 Comments

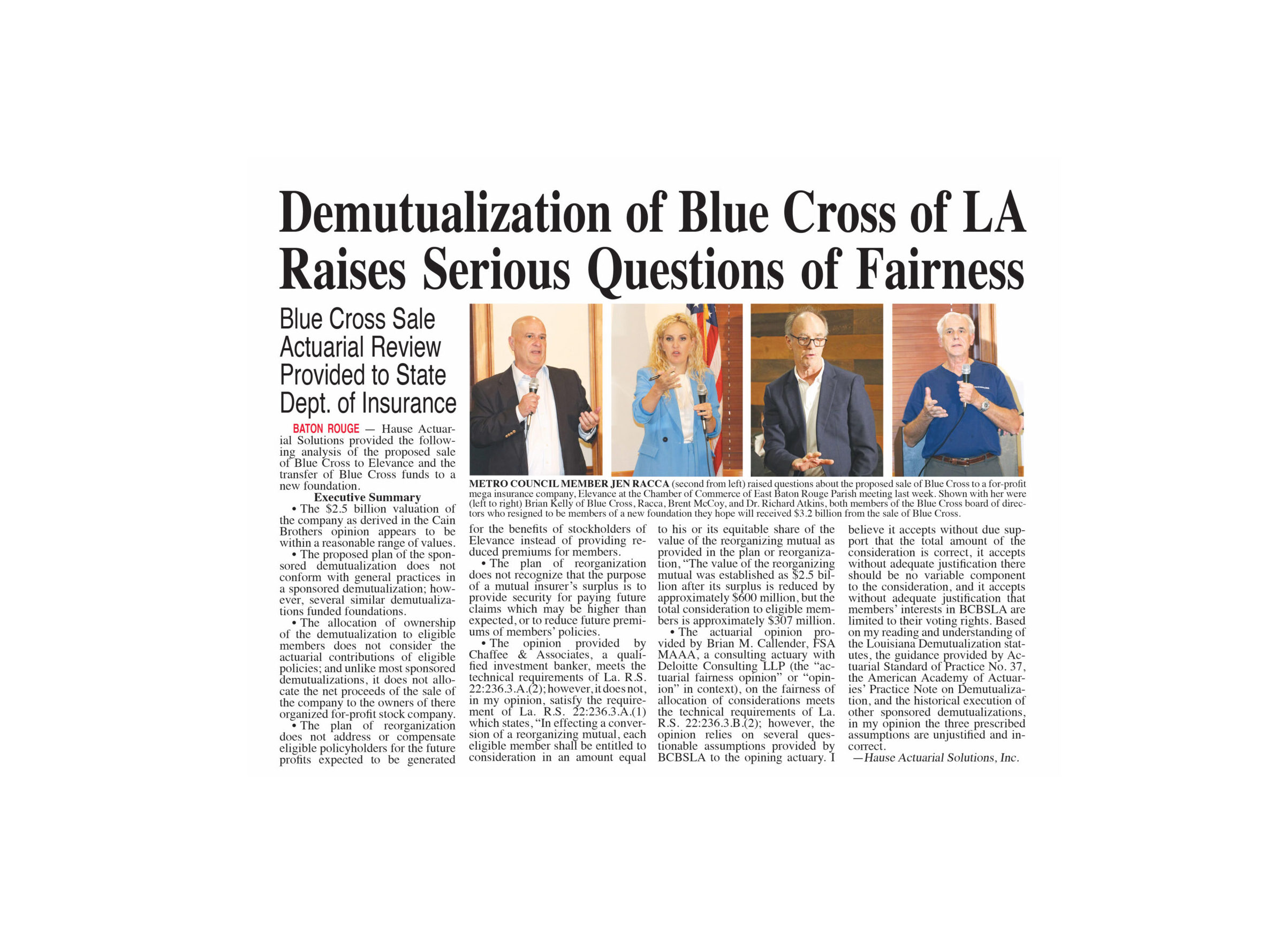

Hause Actuarial Solutions provided the following analysis of the proposed sale of Blue Cross to Elevance and the transfer of Blue Cross funds to a new foundation.

Executive Summary

•The $2.5 billion valuation of the company as derived in the Cain Brothers opinion appears to be within a reasonable range of values.

•The proposed plan of the sponsored demutualization does not conform with general practices in a sponsored demutualization; however, several similar demutualizations funded foundations.

•The allocation of ownership of the demutualization to eligible members does not consider the actuarial contributions of eligible policies; and unlike most sponsored demutualizations, it does not allocate the net proceeds of the sale of the company to the owners of there organized for-profit stock company.

•The plan of reorganization does not address or compensate eligible policyholders for the future profits expected to be generated for the benefits of stockholders of Elevance instead of providing reduced premiums for members.

•The plan of reorganization does not recognize that the purpose of a mutual insurer’s surplus is to provide security for paying future claims which may be higher than expected, or to reduce future premiums of members’ policies.

•The opinion provided by Chaffee & Associates, a qualified investment banker, meets the technical requirements of La. R.S. 22:236.3.A.(2); however, it does not, in my opinion, satisfy the requirement of La. R.S. 22:236.3.A.(1) which states, “In effecting a conversion of a reorganizing mutual, each eligible member shall be entitled to consideration in an amount equal to his or its equitable share of the value of the reorganizing mutual as provided in the plan or reorganization, “The value of the reorganizing mutual was established as $2.5 billion after its surplus is reduced by approximately $600 million, but the total consideration to eligible members is approximately $307 million.

•The actuarial opinion provided by Brian M. Callender, FSA MAAA, a consulting actuary with Deloitte Consulting LLP (the “actuarial fairness opinion” or “opinion” in context), on the fairness of allocation of considerations meets the technical requirements of La. R.S. 22:236.3.B.(2); however, the opinion relies on several questionable assumptions provided by BCBSLA to the opining actuary. I believe it accepts without due support that the total amount of the consideration is correct, it accepts without adequate justification there should be no variable component to the consideration, and it accepts without adequate justification that members’ interests in BCBSLA are limited to their voting rights. Based on my reading and understanding of the Louisiana Demutualization statutes, the guidance provided by Actuarial Standard of Practice No. 37, the American Academy of Actuaries’ Practice Note on Demutualization, and the historical execution of other sponsored demutualizations, in my opinion the three prescribed assumptions are unjustified and incorrect.

—Hause Actuarial Solutions, Inc.

No comments yet... Be the first to leave a reply!